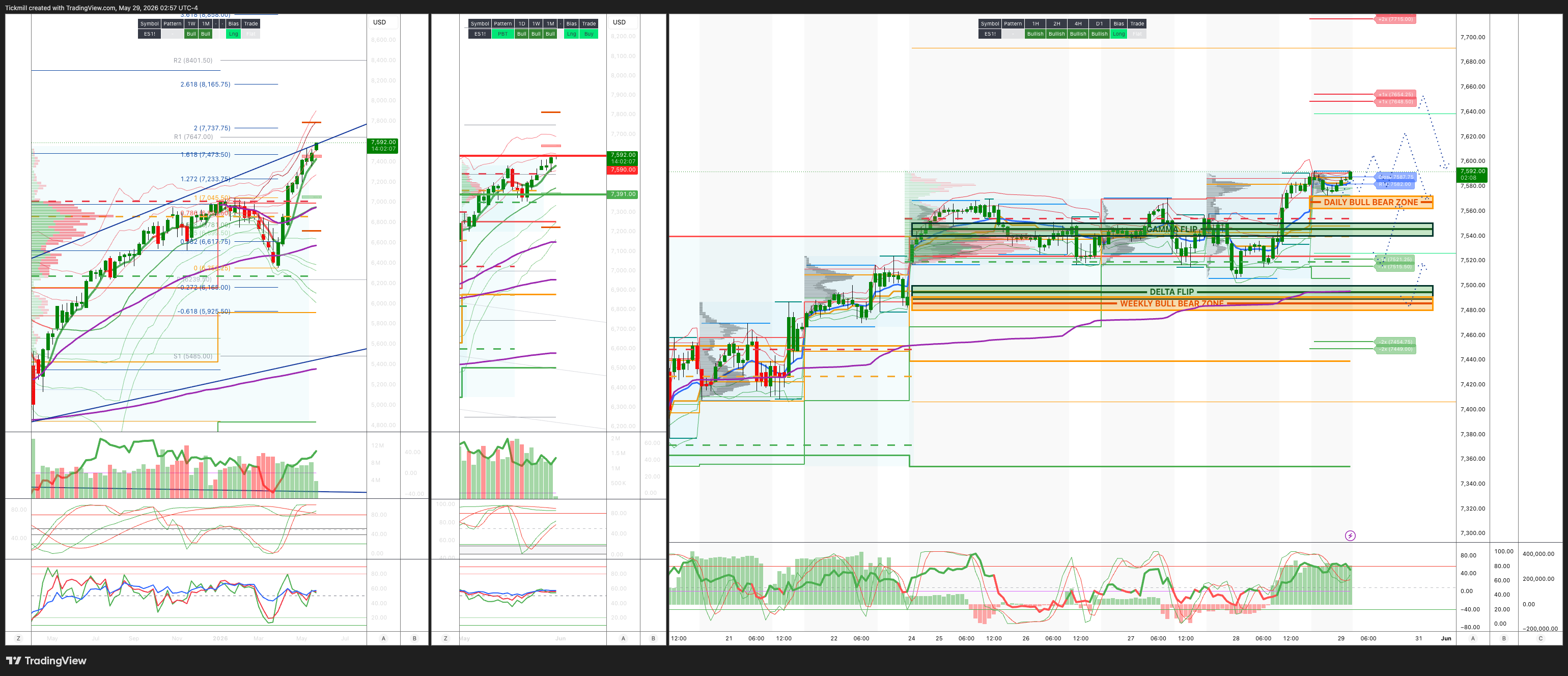

S&P500 Daily Action Areas & Price Targets 29/5/26

S&P500 Daily Action Areas & Price Targets 29/5/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7490/80

WEEKLY RANGE RES 7590 SUP 7391

June MOPEX Straddle: 274pt range implies a OPEX to OPEX range of [7134, 7683]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.15 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BULLISH 7506

WEEKLY VWAP BULLISH 7417

MONTHLY VWAP BULLISH 6898

DAILY STRUCTURE - OTFH 7525

WEEKLY STRUCTURE – OTFH

MONTHLY STRUCTURE - OTFH - 6514

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7560/70

GAMMA FLIP 7544

DELTA FLIP 7495

DAILY RANGE RES 7606 SUP 7488

2 SIGMA RES 7606 SUP 7407

VIX BULL BEAR ZONE 19

TRADES & TARGETS

LONG ON ACCEPTANCE ABOVE DAILY BULL BEAR ZONE TARGET DAILY RANGE RES

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Unwindy’

US Market Recap: Rally Expands Beyond Big Tech

US stocks moved higher again as easing geopolitical concerns and short-covering supported risk sentiment. The S&P 500 rose 0.58% to 7,564, helped by a strong market-on-close buy imbalance. The Nasdaq 100 gained 0.84% to 30,224, the Russell 2000 added 0.57% to 2,937, and the Dow was little changed, up 0.05% to 50,669. Trading volume came in slightly above the year-to-date average.

Markets reflected a broader risk-on tone across asset classes. The VIX dropped to 15.74, the 10-year Treasury yield eased to 4.45%, and the US dollar index slipped to 99.02. Gold advanced, WTI crude held mostly steady after recent declines, and Bitcoin remained under pressure.

The main driver was a combination of improving headlines around the Middle East and a sharp squeeze in under-owned areas of the equity market. Leadership rotated away from crowded winners and into laggards, with software standing out the most. After strong signals from key earnings reports, the software group rebounded sharply, suggesting investors are starting to widen the AI trade beyond chips and infrastructure into software, data, security, and monetization themes.

Short-covering also played an important role. The most-shorted names rallied strongly, reinforcing the view that investors had built up significant hedges and bearish exposure. As geopolitical fears eased, some of that protection was forced to unwind, adding fuel to the move higher.

After the close, earnings added to the momentum. MongoDB jumped after a solid report, Dell surged on strong AI server demand and raised guidance, and Okta gained on a favorable earnings reaction. Together, these moves supported the idea that interest is returning to enterprise software and that AI leadership is broadening rather than replacing the hardware story.

Consumer stocks remained mixed. Some retailers and staples names beat expectations and lifted peers, while weaker results from Burlington showed that spending trends are still uneven. The sector remains highly selective, with company execution continuing to matter more than the macro backdrop alone.

On the flow side, hedge funds turned net buyers after selling in the prior session, with demand focused on macro products, consumer discretionary, and technology. Asset managers were modest net sellers, mainly in financials and consumer discretionary. That shift suggests fast money was pulled back into risk as the squeeze intensified.

In derivatives, downside protection demand eased as equities rose and implied volatility fell. Skew declined across major indices, especially in the Russell 2000 and S&P 500, reflecting reduced demand for hedges and growing interest in upside participation. Options activity pointed to buying in semiconductors, software, healthcare, and select China-related names.

Looking ahead, scheduled macro catalysts are limited, so markets remain highly sensitive to geopolitical headlines.

Options imply a near-term S&P 500 move of about 0.47%, or roughly 36 points, placing the expected range around 7,528 to 7,600. A move above that range could trigger further short-covering and upside chasing, especially in software and heavily shorted stocks. A break below it would likely revive concerns around crowded positioning and bring downside hedging demand back into focus.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!