Dollar Slips On Softer Inflation Data & Ceasefire Extension News

Weaker Inflation Data

The US Dollar has reversed sharply from yesterday’s highs, weighed on by softer US data and news of a ceasefire extension between the US and Iran. On the data front, core PCE yesterday came in at 0.2% month over month, below the prior and expected 0.3% the market was looking for. Prelim q/q GDP was also softer than forecast at 1.6% vs 2% expected, though up from the prior 0.7% reading. Finally, weekly jobless claims were seen rising to 215k from 210k prior, above the 211k the market was looking for. While rate hike expectations were left broadly unchanged on the back of the data, chatter suggests that traders are waiting to see the next CPI figure before committing more fully to the prospect of a hike this year.

US/Iran Ceasefire Extension

Away from the data, the big news was that the US and Iran have agreed to a 60-day extension of the ceasefire, to allow for further negotiations. However, it is unclear yet whether the Strait of Hormuz will be reopened during the ceasefire window. If reopened, this should be firmly bearish for crude prices, pulling USD lower accordingly, as supply improves. However, if the Strait doesn’t reopen and the status quo remains, this could see USD start to move higher again as oil prices rebound. As such, incoming headlines regarding the Strait will be key to near-term USD direction.

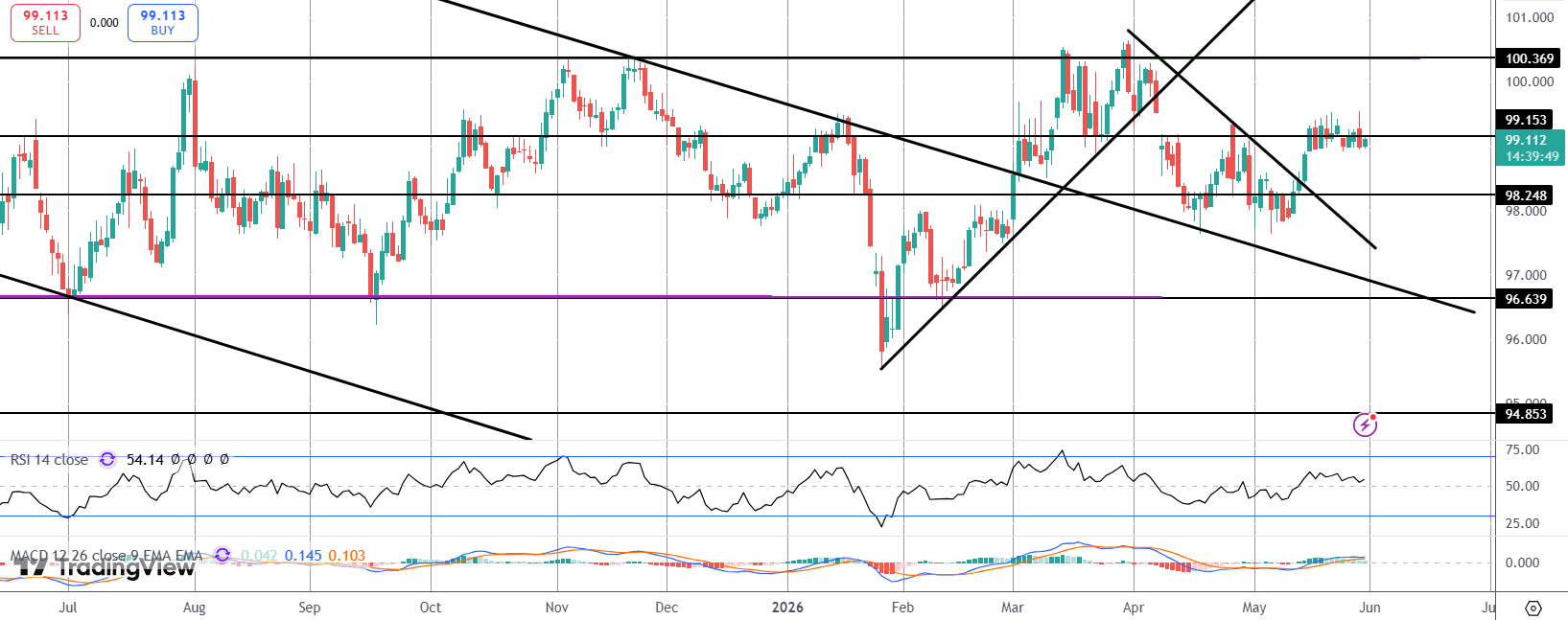

Technical Views

DXY

For now, the index remains glued to the 99.15 level where we’ve seen a tight block of consolidation over recent weeks. If we break higher from here, 100.36 is the next target for bulls. Alternatively, to the downside, 98.24 is the next support to watch.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

With 10 years of experience as a private trader and professional market analyst under his belt, James has carved out an impressive industry reputation. Able to both dissect and explain the key fundamental developments in the market, he communicates their importance and relevance in a succinct and straight forward manner.