Institutional Insights: UBS US Equity Positioning

Over the past few weeks, risk assets have staged a sharp recovery, with many of the market’s key leadership groups — including AI beneficiaries, semiconductors, and technology hardware — now trading well above their pre-conflict levels. Return data from hedge funds suggest that managers have participated meaningfully in the rebound, but broader positioning measures indicate that overall net exposure still has not fully caught up with price action.

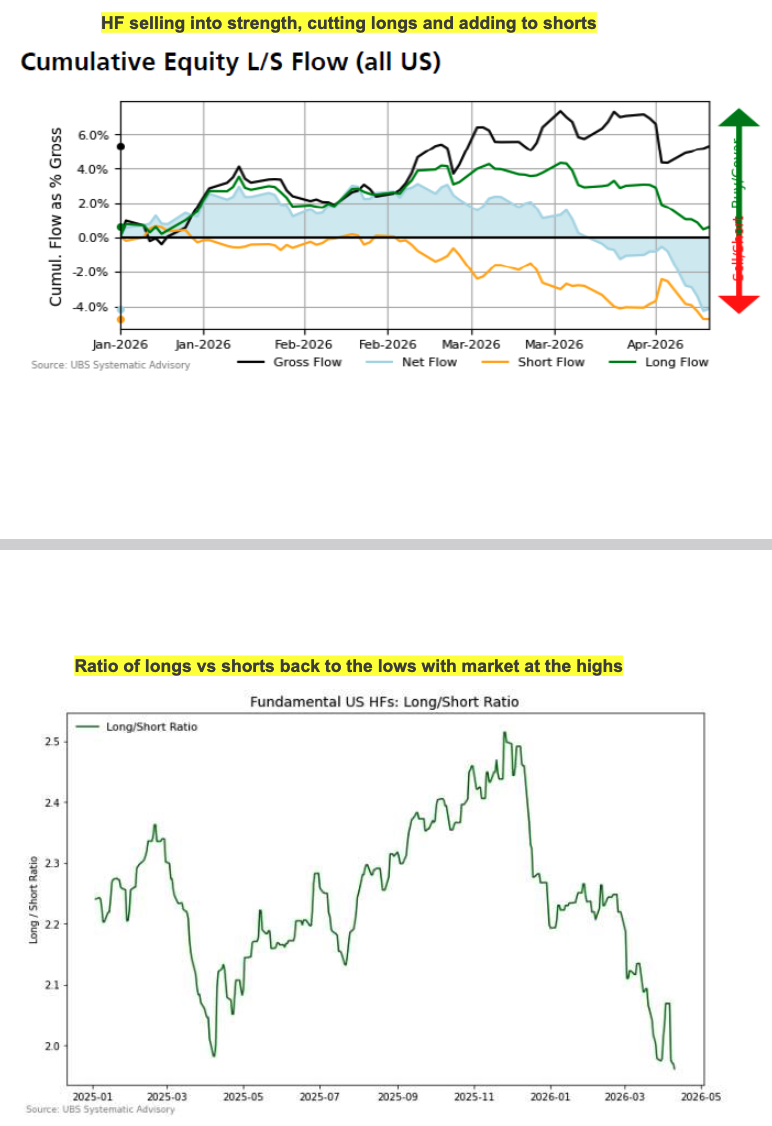

Last week, hedge fund flow data showed the largest net selling of the year so far, driven by a combination of long liquidation and new shorting. On the long side, selling was concentrated in US technology hardware, likely reflecting profit taking after the strong rebound. On the short side, the focus was US software. Despite the recent rally, the aggregate long/short ratio remains near the lows, indicating that exposure remains relatively restrained.

Hedge funds were not the only source of supply. UBS retail flows also recorded their largest weekly outflows of the year, with selling heavily concentrated in semiconductors. More broadly, aggregate discretionary manager positioning still points to only a modest overweight in equities, rather than an aggressively extended long.

Within systematic strategies, CTAs have been the main source of demand. They moved from net short last week to net long, although their current exposure remains only around the 31st percentile, suggesting there is still room for further buying if the market continues to grind higher. By contrast, Risk Control strategies have yet to become meaningful buyers, with exposure essentially unchanged week-on-week because elevated realised volatility is still constraining their models. If market gains become less violent and the S&P 500 averages daily moves of around ±0.50%, Risk Control funds could potentially buy around $185bn over the next month.

When considered together, the positioning backdrop still suggests that equities are likely to continue their upward trajectory, as long as geopolitical risks do not escalate again. In the near term, however, corporate earnings are likely to be the main test for the rally. The options market is currently implying an average move of 5.3% this earnings season, which is only modestly above historical norms, although Technology, Industrials, and Materials are carrying the largest relative event premia.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!