Institutional Insights: Goldman Sachs SP500 Sentiment & Positioning Update 2/6/26

US equities kept climbing, with the S&P 500 posting a ninth straight weekly gain, up 1.4% on the week and 5.0% in May. The rally remains impressive given persistent concerns around geopolitics, private credit, AI-related labor disruption, narrow leadership, equity supply, and political uncertainty. Even so, strong earnings, steady inflows, retail demand, systematic buying, and aggressive buybacks continue to support the market. The key takeaway is that the advance remains healthy, but much of the buying appears to be coming from flow-driven rather than traditional discretionary investors.

Hedge funds added risk again and are now running high net exposure, particularly in fundamental long/short books. Gross and net leverage both moved higher, suggesting managers remain directionally bullish even if overall long/short balances are not extreme. That leaves the market supported in the near term, but also more vulnerable if a negative catalyst forces funds to cut exposure quickly.

Globally, hedge funds were net buyers of equities, driven mostly by long purchases. North America and Emerging Asia led demand, while Europe lagged. Both macro products and single stocks were bought, showing that funds are adding broad market exposure while also selectively increasing stock-specific risk. At the sector level, Financials, Consumer Discretionary, and Health Care saw the strongest buying, while Technology experienced notable de-grossing. That matters because Tech positioning remains structurally elevated, but recent data suggest some trimming after a powerful run.

In Europe, hedge funds remained relatively constructive versus benchmark weightings, but recent flows were mixed rather than clearly bullish. At the same time, North America remains underweight on the Prime book, reinforcing the idea that US market strength is being sustained less by discretionary institutional buying and more by retail, systematic strategies, and corporate demand.

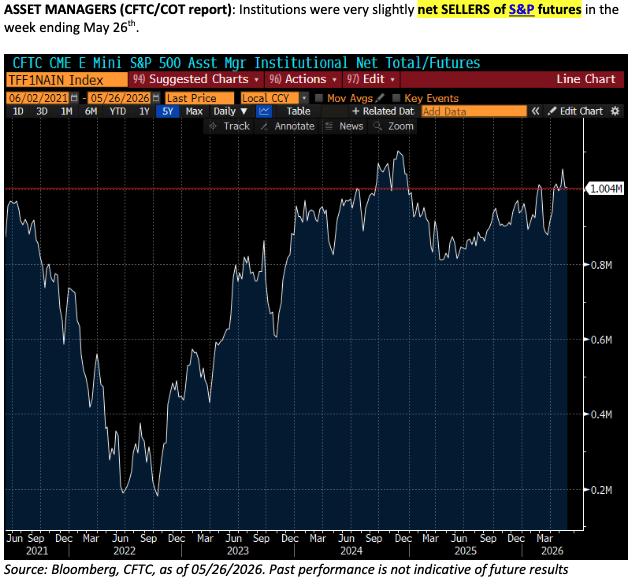

Long-only investors were broadly neutral. Asset managers were slight net sellers of S&P futures, and mutual fund flows globally turned mildly negative. US equity funds still attracted demand, but Europe, Japan, and parts of emerging markets saw outflows. This suggests traditional institutional investors are not aggressively chasing the rally.

Retail remains one of the strongest supports for equities. Individual investors continue to buy despite high valuations, concentration risk, and strong recent gains in Tech and AI-related names. This helps explain why the market can keep making highs even while institutional participation feels muted. It also helps explain the intense speculative activity in areas such as software and other momentum-heavy segments.

Systematic strategies also remain supportive. CTA positioning has increased, and model estimates suggest these funds are still likely to be modest buyers over both short- and medium-term horizons. With the S&P 500 still comfortably above key trigger levels, systematic demand should remain a tailwind unless the market experiences a significant pullback.

Corporate buybacks remain another major pillar of support. Even with heavy equity issuance, buyback execution has been running at very strong levels, especially in Technology, Financials, and Consumer Discretionary. However, this support may weaken later in June as the Q2 blackout window approaches. Pre-arranged 10b5-1 plans should soften the decline, but discretionary buyback activity is still likely to slow.

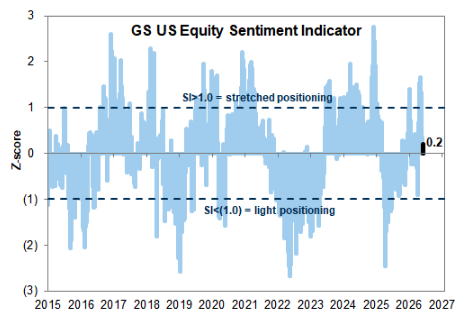

Sentiment is constructive but not euphoric. Survey data show investors remain more cautious than exuberant, and broader sentiment indicators are still near neutral. That backdrop supports the idea of a continued grind higher rather than an overheated melt-up. Still, crowding remains evident in specific areas, especially large-cap Tech and AI-linked momentum trades.

Overall, the market still has multiple sources of support: hedge funds are adding exposure, retail buying remains strong, CTAs are still constructive, and corporations are buying back stock aggressively. The bigger concern is not a lack of buyers, but the nature of those buyers. Much of the demand is driven by flows that may be less sensitive to valuation but can reverse quickly if volatility rises, macro data disappoint, or buyback activity fades.

For the week ahead, that leaves the market in a familiar balance. Strong flow support and solid earnings momentum continue to favor further upside, but investors also face a busy macro calendar, elevated factor volatility, stretched Tech positioning, and the risk of reduced buyback support later this month. The most likely path is still higher, but probably at a slower, choppier pace, with more rotation beneath the surface and less straightforward leadership from the largest Tech winners.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!