Institutional Insights: Goldman Sachs 'Crypto Need To Know'

Market snapshot (spot, flows, macro)

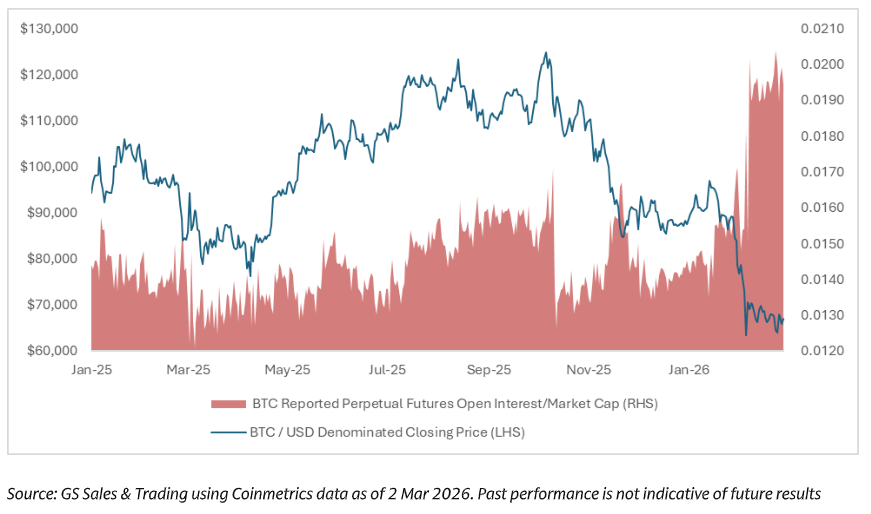

Crypto had a risk-off to reversal to fade week, with spot showing strong absorption of a weekend geopolitical shock.

BTC: ~68k → weekly low ~62.5k (Mon/Tue) → rebound near 70k (Wed) → drift back to mid-60ks by Fri close.

ETH: broadly tracked BTC; mostly 1.8k–2.1k range, ending near 1.9k on Fri.

Cross-asset context: early-week selloff coincided with weakness concentrated in software (AI-related concerns). USD and gold were strong into Monday.

Flows and primary catalyst

ETF flows were the clearest driver of the mid-week bounce.

Spot BTC ETFs: +787m net inflow on the week, breaking a 5-week streak of net outflows.

Key day: +506m net inflow on Wednesday (largest since early Feb), coinciding with BTC’s reversal toward ~70k.

Read-through: spot demand (ETF channel) helped stabilize price even as derivatives remained cautious.

Weekend geopolitical move (liquidity stress test)

Event: coordinated U.S./Israel strikes on Iran (Saturday). Crypto traded as one of the only large liquid markets open.

BTC: fell ~5% (66k → 63k), recovered back toward ~66k same day, rallied above 68k on Sunday (about +8% low-to-high), then settled around ~66k into Monday open.

ETH: fell ~5% (1930 → 1830), rallied to ~2040 on Sunday (about +11% low-to-high), stabilized around ~1950 into Monday open.

Traditional havens: USD and especially gold extended gains (gold ~5260 → above 5400, ~+3%) into Monday.

Takeaway: despite thin weekend liquidity, spot showed solid absorption capacity (fast recovery after the initial selloff).

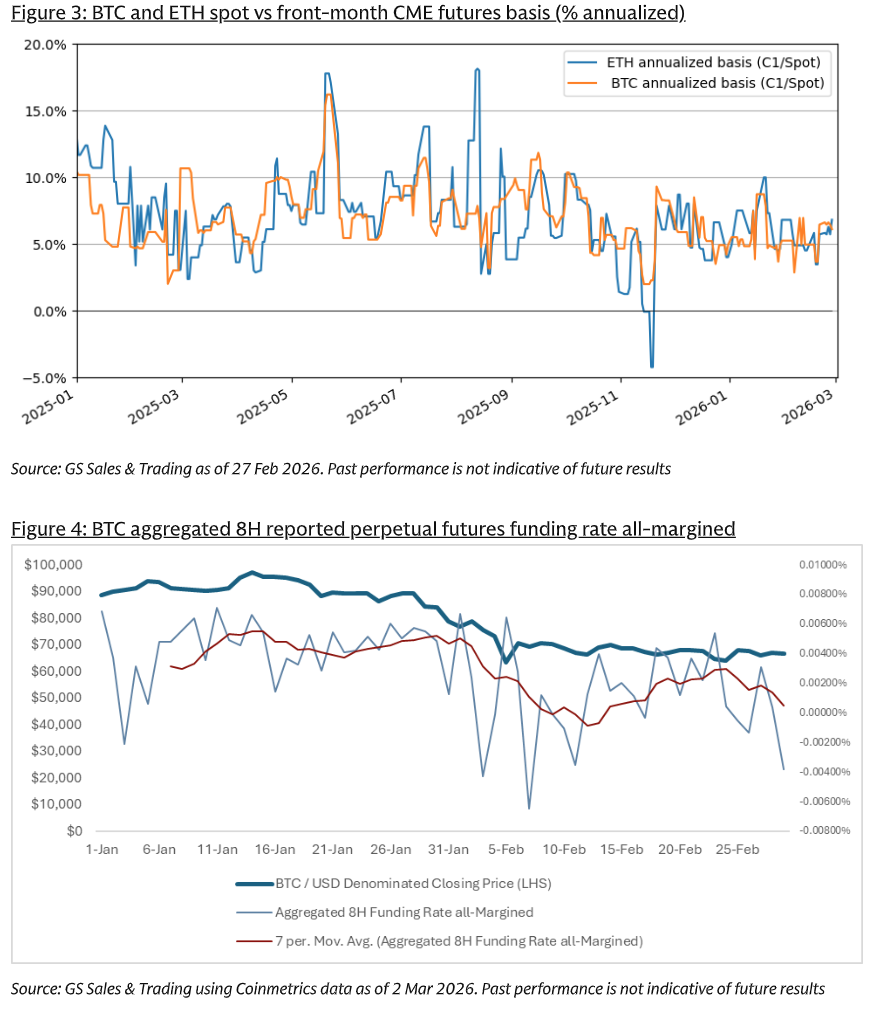

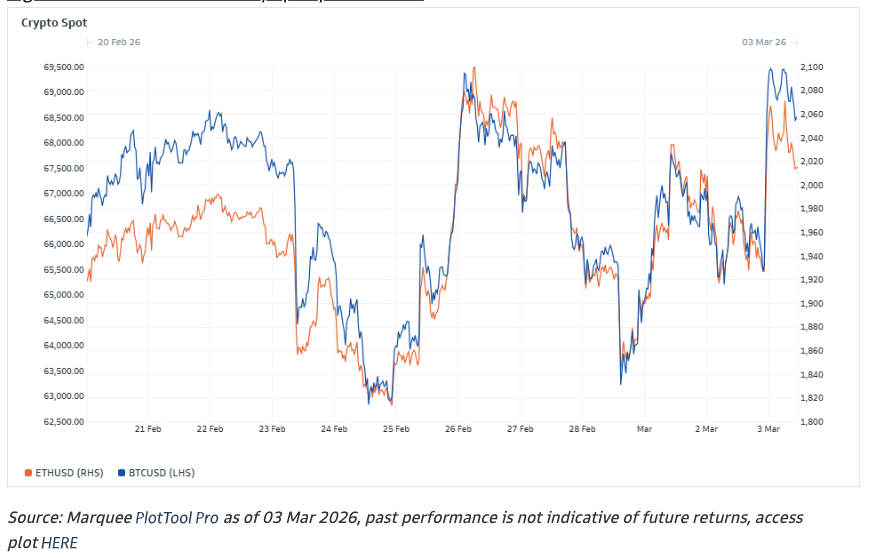

Derivatives (basis, funding, positioning)

Derivatives markets looked more defensive than spot.

CME futures basis

Front-month BTC and ETH futures premium ticked up toward ~6% annualized (from ~4–5%).

Rest of the curve broadly around ~5%.

Perpetual funding (crypto-native venues)

Funding trended lower and dipped negative.

Interpretation: CME basis firming suggests some improvement in institutional carry tone, while negative perp funding points to cautious/short-leaning positioning among crypto-native participants.

Options (vol and skew)

Options continued to price defensive risk despite spot being roughly unchanged over the weekend on a net basis.

Front-month implied vol repriced about +5 vols:

BTC to ~53 vol

ETH to ~72 vol

3m 25-delta risk reversals remained for puts (put-skew persistent).

Example: BTC 3m 25d risk reversal widened to ~8.5 vols for puts at the ~62.5k low, then ended around ~6.5 vols.

Interpretation: traders paid for near-term protection and maintained downside hedges, consistent with risk-off reflexes.

Trading takeaways

Spot looked more constructive than derivatives: ETF inflows and weekend rebound vs negative perp funding and persistent put-skew.

62.5k area mattered: it was the weekly low and where downside hedging demand intensified.

Front-end risk premium rose: higher near-term IV implies the market expects continued choppiness and/or is pricing event risk.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!